Listen now

.svg)

VCs have poured billions into capital-intensive categories—defense, space, data centers—and generated venture-scale returns. So why did wireless, arguably the most critical physical layer of the modern economy, seem un-investable for the last two decades?

The answer was never capital intensity. It was a fundamentally broken market structure for VC economics. Telecom had a venture math problem no product brilliance could solve: a handful of carrier customers, multi-year sales cycles through standards bodies, and an exit path that ran exclusively through the incumbents whose stack you were augmenting. In VC terms, imagine your TAM is five customers, your sales cycle is three years, and your only acquirer is also your platform dependency. That’s been the challenge of wireless, where promising technologies like Sigfox, Parallel Wireless, and Kumu failed because of brutal adoption cycles, not product quality.

What’s changed?

AI is becoming ubiquitous—and mobile. Every major AI platform now requires continuous connectivity to deliver real-time intelligence at the device level. Whether that's a smartphone, AR headset, or another hardware modality, a network dead zone is no longer a dropped call. It's a broken product. With nearly half of ChatGPT’s 900M weekly users accessing it over mobile, connectivity becomes the first requirement. The largest mobile platforms are already responding. Google partnered with Skylo, and Apple secured the vast majority of Globalstar’s capacity. That partnership continues even after Amazon’s acquisition of Globalstar, extending connectivity beyond terrestrial networks. These are not traditional telecom plays. They are connectivity plays.

Ubiquitous connectivity is only part of the story. Gemini embedded into the core Android OS, Apple Intelligence providing real-time analysis of the physical world, frontier labs pushing voice as the primary interface. All have fundamentally changed what users expect from wireless. Networks architected for static consumption were never designed for dynamic reasoning workloads, real-time voice agents, or hybrid inference splitting computation between device and cloud. The deeper problem isn't just throughput. It's that AI changes the shape of the traffic itself: intermittent, event-driven, uplink-heavy as users shift from consuming content to creating and sensing. A demand profile evolving at software speed is colliding with an architectural model that still moves in generational cycles. Just as AI has forced a generational rearchitecting of the data center, it's now reshaping the requirements for wireless networks.

Though early, the Open Radio Access Network movement (O-RAN) created the first real opening in a closed stack. Paired with surging AI demand, a new generation of startups is emerging to transform how wireless networks are built and delivered. The market is starting to reflect the shift. Since 2024, HPE acquired Juniper Networks for $14 billion to build "AI-native networking," while NVIDIA, AWS, Microsoft, and Google have become active investors in wireless innovation. The commercial dynamics that kept VCs away may be starting to change.

So where are we heading? The beginnings of an architectural redesign for ubiquitous AI. When NVIDIA invested $1 billion in Nokia in October 2024, for example—betting the base station is the next GPU-accelerated platform—it signaled that the largest technology companies see wireless as a strategic asset to reshape. That bet is already producing results. In March 2026, Nokia and NVIDIA completed functional tests of concurrent AI and RAN processing on shared GPU infrastructure with major operators. Zooming out, the venture opportunity is in the intelligence and software layers that make this type of communication infrastructure programmable and adaptive. The control plane for an AI-native wireless world.

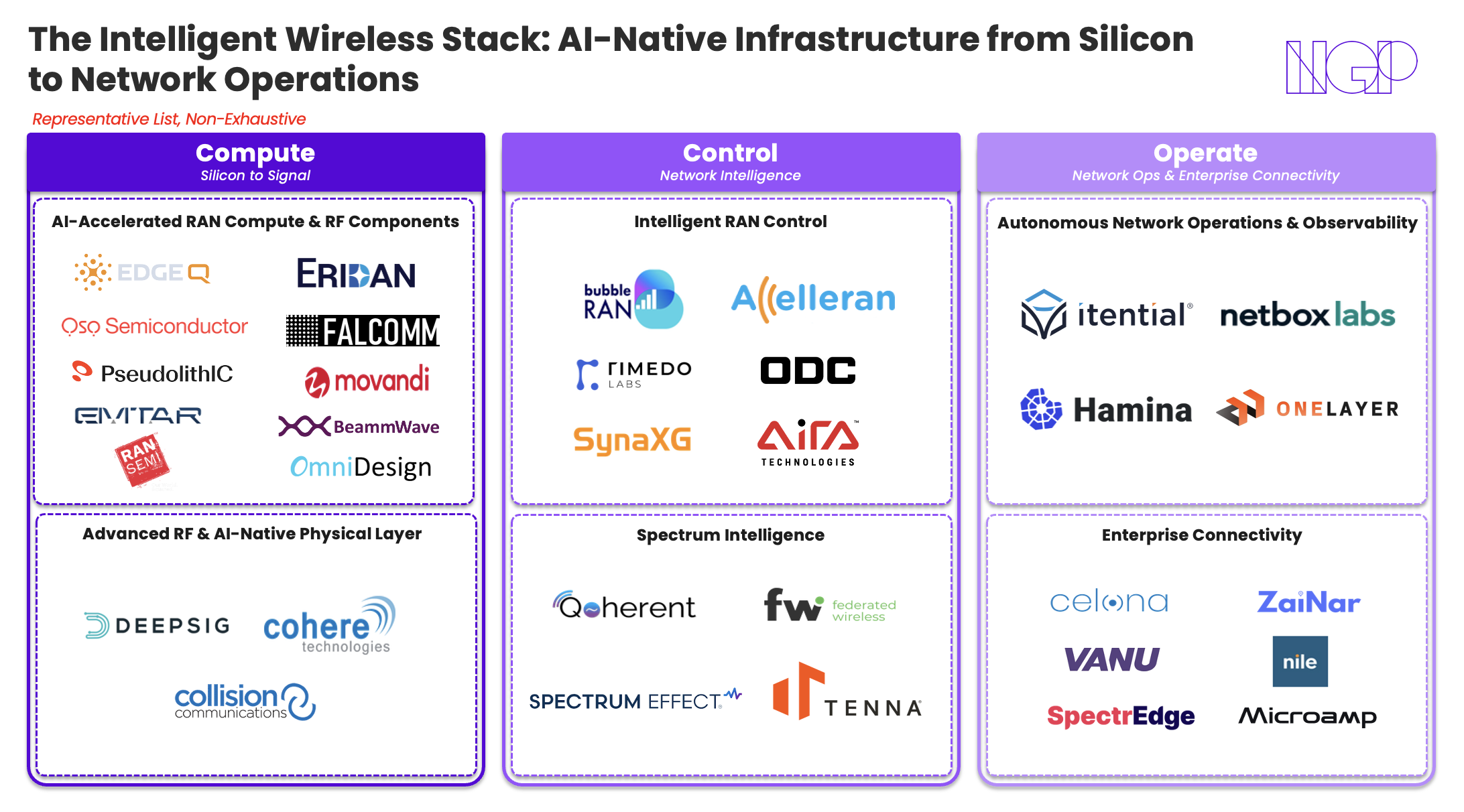

What the New Stack Actually Looks Like

The founders we're excited about aren't building better versions of legacy hardware. The opportunity spans three layers of the stack: new compute that unifies wireless and AI processing, intelligent software that optimizes network performance and spectrum in real time, and autonomous operations that replace manual network management entirely.

At the silicon layer, a new generation of chips is unifying 4G, 5G, and inference on a single programmable system-on-chip. In the radio and network intelligence layer, rigid hand-coded signal processing algorithms are giving way to neural receivers and AI-driven optimization. On top of the stack, AI-native platforms are emerging to automate network operations across increasingly complex systems.

Why This Moment Is Different

It’s still early. No startup building intelligent networking technology has seen a >$B outcome, and the shift to AI-RAN is still in its infancy. What separates this moment is that pressure is arriving from outside telecom, demanding use cases that existing networks were never designed to serve.

On-device AI is turning every smartphone into a local reasoning engine. Meanwhile, physical AI is scaling quickly with autonomous vehicles, industrial robots, and drone fleets each demanding reliable wireless that static networks cannot guarantee. The network must now orchestrate every workload between device, edge, and cloud in real time. Together, these create a commercial forcing function that didn't exist two years ago.

At NGP Capital, we've continued to invest in the next generation of connectivity through Skylo and Xona, and in taming the complexity of these networks through NetBox Labs. The founders who define the next decade will win by making wireless networks as programmable and adaptive as the AI workloads they carry. The era of ubiquitous intelligence is arriving. Is this finally the right moment to back the leaders reshaping how it's delivered?

If you’re building the connective tissue for this new era—from silicon and spectrum intelligence to AI-native NetOps—I’d love to chat eric@ngpcap.com!

Related articles

Global logistics – an industry in transition

Unveiling the future: Can SaaS successfully bounce back in 2024?

Paul Asel on TechCrunch: "The changing nature of venture capital"

Related articles

AI’s aha moment: AI inference

AI is scaling beyond the Cloud, towards the Edge

How to critically think about the AI frenzy