Listen now

.svg)

SaaS companies were tested in 2023 with average growth rates falling below 20%, ushering in a new era focused on profitability. In this period of recalibration, average public SaaS revenue multiples stayed in a tight range of roughly 6-8x, a stark contrast to the 8-year trailing average of 13x and the 2021-22 peaks of over 20x. Stabilizing interest rates and economic growth set a promising outlook for 2024. In this article, we dissect the performance and valuation of over 90 SaaS companies trading on the Nasdaq and New York Stock Exchange to assess the driving factors behind valuation multiples and the likelihood of a rebound in the SaaS landscape for 2024.

The Macroeconomic Landscape

In 2023 SaaS businesses felt the sting of a turbulent economy - characterized by rising interest rates, high inflation, and a slowdown in growth. To combat inflation, which reached a staggering peak of 9.1% in June 2022, the U.S Federal Reserve Board (Fed) raised interest rates a whopping 5.25 percentage points (from 0.25% to 5.50%) over the last two years across eleven interest rate hikes. This constitutes the fastest and most severe tightening cycle since the 1980s. As the economy continued to grow and inflation cooled to 3.1% (CPI as of November 2023), the Fed paused interest rate hikes leaving the upper limit at 5.50%. In December 2023, the S&P 500 and the NASDAQ rose 4% and 6%, respectively and the indices rose 22% and 43% respectively for the full year. Heading into 2024, improving economic conditions and stable (or declining) interest rates could catalyze stock market growth, which would in tandem boost the average revenue multiples for SaaS companies.

Public SaaS Company Performance in 2023

Across the studied group of SaaS companies, the pace of growth slowed in 2023 with the average revenue growth rate dropping to 18% for 2023E, compared to 21% in 2022 (note: 2023E refers to the mid-range forecast for 2023 as of Q3 2023). Top quartile growth rates faced a more pronounced reduction, dipping to 23% from 28% in 2022. As companies struggle to maintain growth rates above 20%, they are shifting attention toward enhancing their bottom line. On average, public SaaS companies anticipated an 8% improvement in their EBITDA margins in 2023. The average EBITDA margin in 2022 was -20% compared to -12% for 2023E. Top quartile EBITDA margins are projected to be positive, at 2.9% in 2023 compared to -1% in 2022.

Leading SaaS companies such as Datadog, ServiceNow, and Hubspot, with top quartile EV/TTM revenue multiples, expected an average growth rate of 26% (top quartile growth) in 2023 with an average expected EBITDA margin of -6% (above median). This suggests a broader perspective that while improving EBITDA margin is important, profitability should not be the sole focus and needs to be balanced with sustained top-line growth. Focusing on optimizing both growth and EBITDA margin and progressing towards the Rule of 40 (achieving a combined growth and EBITDA margin of 40%) is likely a winning strategy for 2024. Interestingly, as of Q3 2023, fewer than 10% of public SaaS companies had achieved the Rule of 40. The average Rule of 40 calculation stands at 9.1%, with a top quartile of 24.9%. Although still below 40%, these figures represent a significant improvement from 2022 when the average was 0.6% and the top quartile stood at 18.6%.

Revenue Multiple Trends for Public SaaS Companies

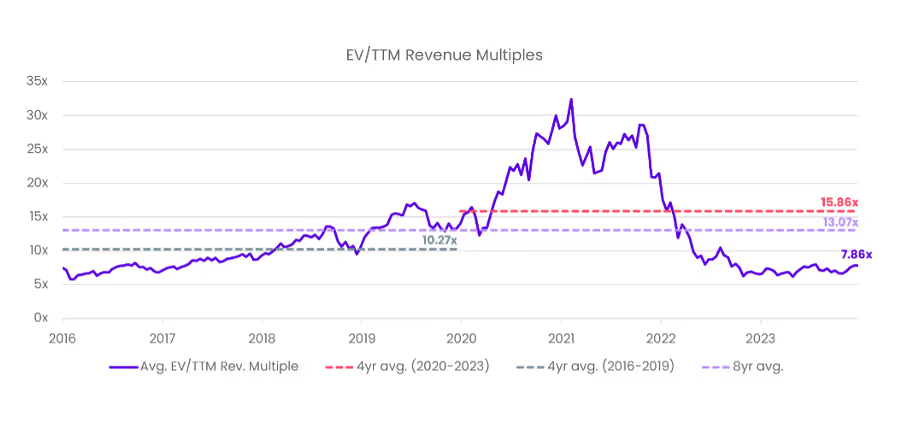

Following the peaks of 2021 and 2022, revenue multiples for SaaS companies descended to levels not seen since 2016 and stabilized in the range of 6-8x. 2023 ended with an average EV/TTM revenue multiple of 7.9x, at the top end of the annual range (6.2x to 8.0x). Current multiples linger below historical averages, with a trailing 8-year average of 13.1x and a pre-COVID average (2016-2019) of 10.3x.

At the close of 2023, top quartile SaaS businesses traded at 10.7x EV/TTM revenue, up from 9.0x at the end of 2022. The cohort of top quartile companies changed materially in 2023, with over a third of 2022’s top quartile companies falling out of the ranking in 2023. These ousted companies were predominantly fast-growing but highly unprofitable businesses with an average 2023E growth rate of 37% and a -17% EBITDA margin. They were replaced in the top quartile by a profitable group of companies with an average growth rate of 20% and a 5% EBITDA margin for 2023E. The shuffle within the top quartile companies underscores the market’s evolving preference toward profitable businesses.

2024 Outlook

As the spotlight shifts to 2024, the trajectory for SaaS valuations appears promising due to renewed optimism around growth and subdued inflation rates. In the public markets, a discernible shift toward prioritizing sustainable profitability is underway signaling a pivotal shift away from the former growth-at-all-costs mindset. While revenue multiples are unlikely to return to the peak levels of 2021 and 2022, there is a sense that coupled with an economic recovery, average multiples could return to or even exceed the 2016-2019 average of 10x.

For private SaaS companies, market valuations often lag public market trends, meaning private companies may have to wait a while longer before seeing a recovery in private SaaS valuations. Privately held SaaS companies are in for a ride as they navigate the waves of public market trends. To snag top-tier valuations in 2024, companies should prioritize efficiency and progress towards the Rule of 40.

Related articles

From the brink of bankruptcy to billion-dollar exit

.png)

Re-imagining satellite navigation: Why we invested in Xona Space Systems

Securing enterprises by providing the objective truth

Related articles

How API-based SaaS is redefining software

Technologies that will reshape our world in 2024: Three predictions

The story of 3 IPOs and what we can learn from it